The Dalai Lama, when asked what surprised him most about humanity, answered: “Man. Because he sacrifices his health in order to make money. Then he sacrifices money to recuperate his health. And then he is so anxious about the future that he does not enjoy the present; the result being that he does not live in the present or the future; he lives as if he is never going to die, and then dies having never really lived.”

We are in the late stage of a long-term debt cycle. Debt has become so high it is difficult to give lender-creditors a high enough interest rate relative to inflation to make them want to hold this debt as an asset without making the rates so high that it hurts the borrower-debtor. The U.S. Treasury will either have to pay higher rates on its giant deficit or print a lot of money to buy bonds thereby devaluing money (inflation).

At the same time, the Federal Reserve has held up on raising rates but has clamped down on the money supply in a big way (see Nick’s Numbers) in what can now be considered quantitative tightening. Despite stubborn positive indicators demonstrating resilience, the state of the money supply and market indicators point toward an impending contraction.

Nick’s Numbers

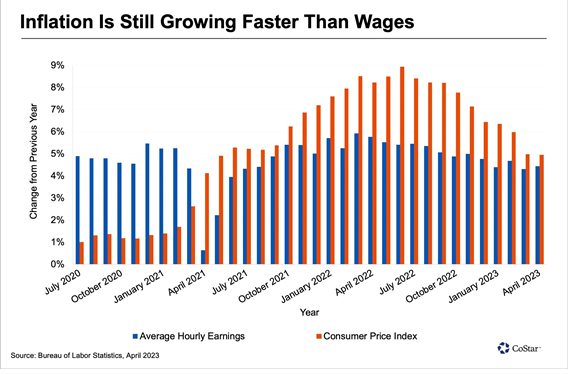

Below is the chart of the M2 (Money Supply) that Don references above. An equally interesting chart is the rate of inflation overlaid with wage increases. The graphic obviously shows that the consumer is not keeping up!

If you would like an analysis of your properties’ value or to discuss what you should be doing with regard to interest rates or inflation and their impacts on your business, tenants, or property, I’d be happy to talk. (Nick Zech, 858-232-2100, nzech@cdccommerical.com).

As Nick also points out, although wages are growing, they are not outpacing inflation. This is forcing households to take on more debt. Outstanding credit card debt rose by 17.2% from Q1 2022 to Q1 2023. At the same time, credit card rates have jumped from 14.6% to 20.1%.

John Rubino, a writer/analyst (perhaps Armageddonist) talks about how household net worth “is illusionary because as we borrow to buy, and assets rise because we all bought and our net worth goes up.” We feel “safer” because of our increased “net worth.” However, the leverage cuts both ways and when asset prices go down, the debt stays the same, or worse, needs to be refinanced at higher rates. Debt only falls as it is paid off. His takeaway is that in a society of borrowers and speculators, asset values increase because of borrowing and speculation, which makes rising household net worth both a negative indicator of future growth and a sign of fragility rather than strength. But until people figure this out, it remains a great tool for convincing consumers that everything is fine when it’s actually not.

This time last year, Sacramento was abuzz like it had won a lottery ticket. They had a $97.5 billion budget surplus! How quickly things change. In less than 12 months, the State now has a $31.5 billion budget deficit! (Where did all of the king’s clothes go?). I am not worried, I am sure they will find a way to tax us for it.

I am not yet sure how they will handle tenants and building owners, but California utility companies are in the process of rolling out a new fixed-rate bill proposal (this is just the monthly charge to be hooked up to the grid – not the electricity used!). The basics of the proposal are the more income you make, the more you pay for the flat rate. Then, there will be reduced usage charges by using the subsidy paid by everyone’s flat rate hookup charge. I believe this is what Robin Hood called, “take from the rich and give to the poor.”

Here’s the breakdown of pricing for San Diegans.

Household income $28,000 – $69,000 would pay $34/month.

Household income $69,000 – $180,000 would pay $73/month.

Household income above $180,000 would pay $128/month.

All these fees are tacked on before using a single kilowatt hour, meaning median-income San Diegans will pay $876 a year in electricity rates, regardless of whether they use any electricity. Also, San Diegans will still get charged these monthly rates if they installed residential solar.

Meanwhile, get on quoting and renewing your property insurance policies early this year. We are seeing a dramatic uptick in non-renewal notices and policy holders scrambling to get insurance coverage.

So, with all of this doom & gloom, you might ask, “How’s the market? How are you guys doing?” To this I would answer, “our 1st quarter was amazing – as good as a good year for us.” The 2nd quarter was so-so. But the 3rd quarter is lining up to be as good as the first! I’ve been scratching my head and I think that the best explanation is we are problem solvers and accept most all challenges. So, we’re busy because there are problems to solve. I used this month’s story 13 or so years ago, but it was too perfect not to use again. Hope you enjoy the story…

Suddenly, a rich tourist comes to town.

He enters the only hotel, lays a 100 Euro note on the reception counter, and goes to inspect the rooms upstairs in order to pick one.

The hotel proprietor takes the 100 Euro note and runs to pay his debt to the butcher.

The butcher takes the 100 Euro note, and runs to pay his debt to the pig grower.

The pig grower takes the 100 Euro note, and runs to pay his debt to the supplier of his feed and fuel.

The supplier of feed and fuel takes the 100 Euro note and runs to pay his debt to the town’s prostitute that in these hard times, gave her “services” on credit.

The hooker runs to the hotel, and pays off her debt with the 100 Euro note to the hotel proprietor to pay for the rooms that she rented when she brought her clients there.

The hotel proprietor then lays the 100 Euro note back on the counter so that the rich tourist will not suspect anything.

At that moment, the rich tourist comes down after inspecting the rooms, and takes his 100 Euro note, after saying that he did not like any of the rooms, and leaves town.

No one earned anything. However, the whole town is now without debt, and looks to the future with a lot of optimism…

And that, ladies, and gentlemen, is how the United States government is doing business today.

Jane Goulart

Monthly Letter Signup

Enter your information above to be added to our Monthly Letter email list.